|

|

ROLEXROLEXROLEXROLEXROLEXROLEX

ROLEXROLEXROLEXROLEXROLEXROLEX

ROLEXROLEXROLEXROLEXROLEXROLEX

22 March 2024, 10:13 AM

22 March 2024, 10:13 AM

|

#31 | |

|

"TRF" Member

Join Date: Oct 2011

Real Name: Seth

Location: nj

Watch: Omega

Posts: 24,856

|

Quote:

That same And costs more money. Not because the value of the house went up. But because the value of the money went down.

__________________

If happiness is a state of mind, why look anywhere else for it? IG: gsmotorclub IG: thesawcollection (Both mostly just car stuff) |

|

|

|

|

22 March 2024, 10:55 AM

|

#32 |

|

"TRF" Member

Join Date: Apr 2015

Location: Minneapolis

Posts: 225

|

|

|

|

|

|

22 March 2024, 04:18 PM

|

#33 | |

|

"TRF" Member

Join Date: Aug 2019

Real Name: Phillip

Location: Right here

Watch: SD43 Daytona Blusy

Posts: 2,173

|

Quote:

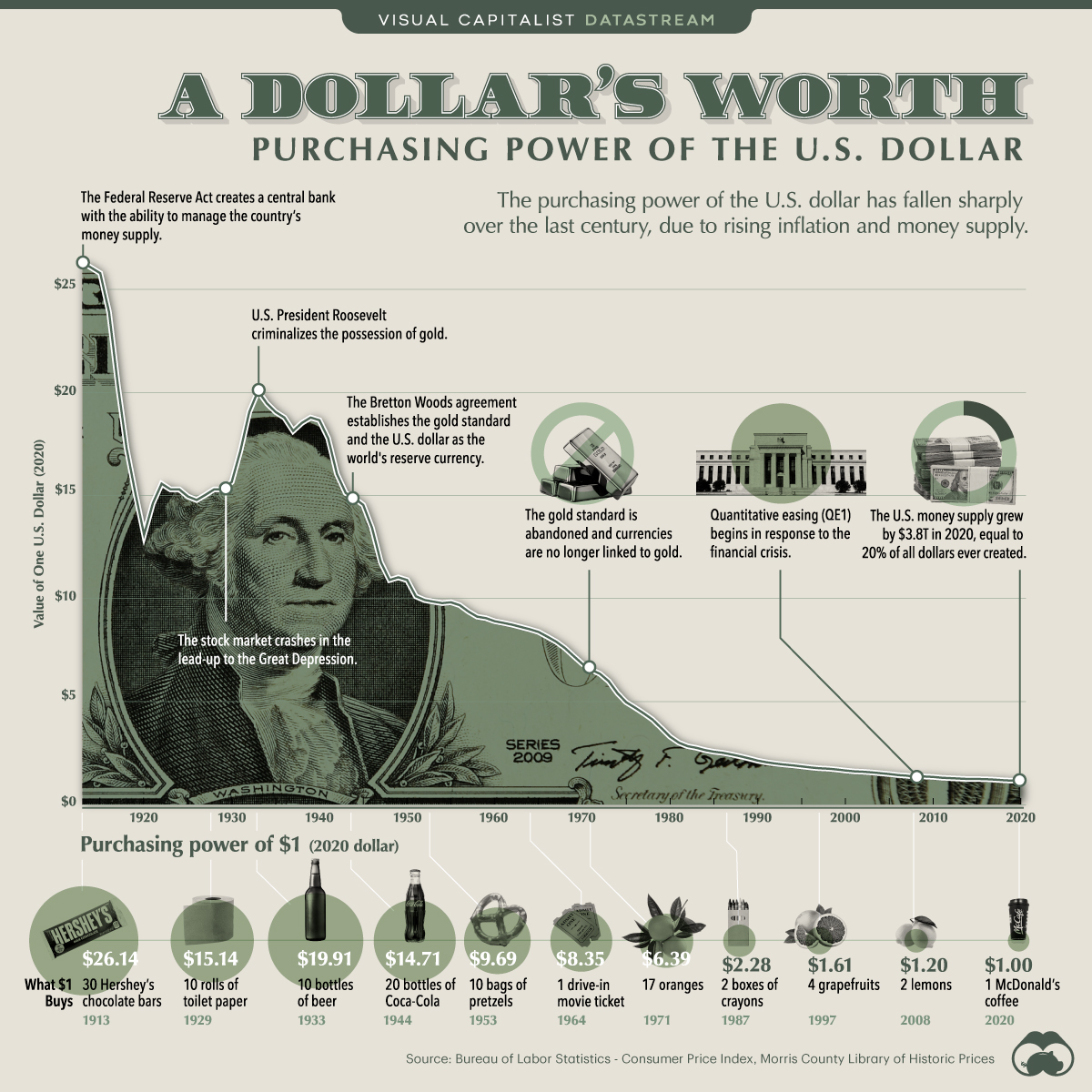

Just 4 years ago, you needed just $59,000 in income to afford the average home. That's a $47,000, or 80%, increase in income from 2020 while wages are up just 23% over that time. Currently, the median HOUSEHOLD income in the US is ~$75,000. In other words, the median household income used to be 27% ABOVE the income needed to afford a home Now, the median household income is 41% BELOW the income needed to afford a home. |

|

|

|

|

|

22 March 2024, 07:26 PM

|

#34 |

|

"TRF" Member

Join Date: Jan 2015

Real Name: Knackers

Location: NI/Aust/USA

Watch: and wait

Posts: 3,386

|

Is this a Homer D oh or just pronounced the same way?

|

|

|

|

22 March 2024, 07:35 PM

|

#35 | |

|

2025 Pledge Member

Join Date: Jul 2013

Real Name: Brian (TBone)

Location: canada

Watch: es make me smile

Posts: 79,357

|

Quote:

|

|

|

|

|

|

22 March 2024, 08:02 PM

|

#36 | |

|

"TRF" Member

Join Date: Jan 2015

Real Name: Knackers

Location: NI/Aust/USA

Watch: and wait

Posts: 3,386

|

Quote:

|

|

|

|

|

|

22 March 2024, 08:52 PM

|

#37 |

|

"TRF" Member

Join Date: Jun 2023

Location: USA

Posts: 1,690

|

I remember back in 89 a Ford Tempo was about $10k. Median HHI about $30k. For 1/3 your median household income you could have a car with cheap seats, few safety features, barely audible FM radio, manual everything (including roll up windows) and a rust guarantee. Guaranteed to rust.

Today, median US HH income is just over $70k. For one third your HH income you get safety systems out the wazoo, an infotainment system, automatic everything, 2x+ the power, the same or better mileage, and a reasonably reliable car. Computing technology is even more dramatic, of course, with people walking around with phones more powerful than servers that were about 100x the cost. The thing many people are missing in these devaluation narratives (and equally uninformative charts) is that productivity matters AND that there are opportunities to invest and earn returns in excess of inflation (real returns). Sure there are major issues - housing prices, but this reflects an expectation that as wealth grows (and populations) fixed production items will inflate more rapidly. As for bubbles today, I have little doubt there are many. Crypto ponzi hype, AI bandwagon, and Tesla are three obvious ones. Tesla is slowly deflating and will eventually price to reality. The others - well, my logic is to focus on smart diversification because irrationality can last a long time… |

|

|

|

|

22 March 2024, 09:05 PM

|

#38 |

|

"TRF" Member

Join Date: Jun 2023

Location: USA

Posts: 1,690

|

Btw, to me the shocking thing about this market is the typical consumer’s appetite to spend past their means. This is (for 75%+ of the population) a decision. Conscious decision? Not sure. But discretionary spend is out of control… compared to my personal view of risk.

But that is by choice. People choosing the $40k or $50k car over the $25k car. Or the branded everything… sure, paycheck to paycheck is real. But largely decision driven for a vast majority when you look at spending patterns. These things can continue for longer than someone more conservative might expect. Entire countries have spend patterns that defy prudent behavior (Canada is a great example). Timing the demise of something that is rooted in psychology, amplified and reinforced… is extremely difficult absent a clear catalyst. Sometimes identifying those catalysts can be tricky because data is ambiguous. I remember making the call that US banks were likely to face distress… back in 2006. A couple years early (nearly an eternity in trading terms). That was with clear and convincing data. Data today around if and when the likely catalyst (depleted savings imho) brings a reckoning… well, it is extremely murky. Everything is dynamic as well - every action has a reaction. A decline in spending will have pronounced impacts on inflation (down) and therefore rates (down). Lots of money is indeed on the sidelines now too… the net effects are impossible to completely understand a priori. Finally, anyone not extremely well versed in using options theory to make investment decisions… I highly recommend getting smart in that area. My 5 cents (inflation-adjusted). |

|

|

|

|

22 March 2024, 10:19 PM

|

#39 | |

|

"TRF" Member

Join Date: Feb 2017

Location: USA

Posts: 4,416

|

Quote:

|

|

|

|

|

|

22 March 2024, 10:44 PM

|

#40 | |

|

"TRF" Member

Join Date: Jun 2023

Location: USA

Posts: 1,690

|

Quote:

Even people who are stretched thin have a lot of stuff already. Sure, much of what they own is on credit, but there is also a decent equity cushion too. Lower income wage growth has risen sharply. The biggest mitigating factor is we finally have a reset in rates to higher levels. There is now a real lever to pull should we need to - this mitigated the near and medium term catastrophe risk substantially. Nevermind the higher income and net worth groups that have tremendous assets. Consider how so many of us have allocations into fixed income products now - as hedges to risk. Consider now if there is a large market correction, how that will be re-allocated The real risks are more government / fiscal in nature. Even there we see situations where greater overall debt (consumer plus governmental) with far less productive assets / weaker capitalist frameworks, manage to avoid reasonable definitions of outright catastrophe So I see a correction coming but timing remains uncertain, duration unlikely to be sustained and magnitude limited. Of course in some bubble segments a bigger drop is probable, but generally speaking Im not worried about doomsday economic outcomes. |

|

|

|

|

|

22 March 2024, 10:56 PM

|

#41 | |

|

"TRF" Member

Join Date: Feb 2017

Location: USA

Posts: 4,416

|

Quote:

|

|

|

|

|

|

22 March 2024, 10:58 PM

|

#42 | |

|

"TRF" Member

Join Date: Oct 2011

Real Name: Seth

Location: nj

Watch: Omega

Posts: 24,856

|

Quote:

Maybe Im just a pessimist. But I think its just been a long burn and a lot of moves to avoid the inevitable.

__________________

If happiness is a state of mind, why look anywhere else for it? IG: gsmotorclub IG: thesawcollection (Both mostly just car stuff) |

|

|

|

|

|

22 March 2024, 11:00 PM

|

#43 | |

|

"TRF" Member

Join Date: Oct 2011

Real Name: Seth

Location: nj

Watch: Omega

Posts: 24,856

|

Quote:

And doing the same in regard to investing new funds. But the funds I have already are safe. Keeping it that way.

__________________

If happiness is a state of mind, why look anywhere else for it? IG: gsmotorclub IG: thesawcollection (Both mostly just car stuff) |

|

|

|

|

|

22 March 2024, 11:03 PM

|

#44 | |

|

"TRF" Member

Join Date: Feb 2017

Location: USA

Posts: 4,416

|

Quote:

|

|

|

|

|

|

22 March 2024, 11:10 PM

|

#45 |

|

"TRF" Member

Join Date: Dec 2021

Location: Asia

Posts: 887

|

All I know is I grew up in a typical middle class family in LA: father worked an office job, mom took care of the house and kids. On a salary well below 6 figures (remember when that used to be the benchmark? It doesn't even sound like much these days), we were able to own a nice house, eat out often, buy toys, and go on multiple vacations per year. Good luck trying to do that now.

I don't envy the generation just starting out now nor their kids. |

|

|

|

|

22 March 2024, 11:20 PM

|

#46 | |

|

"TRF" Member

Join Date: Jun 2023

Location: USA

Posts: 1,690

|

Quote:

Michael Burry is worth listening to. Often wrong in conclusions but sound analysis - one of those whose views are worth my attention, even if I ultimately disagree. As for staying the course, I think over most extended (but reasonable) modern periods this is the right strategy. There is also the value of matching strategy to your own psychology. Being constantly stressed over risks, even if rationally the risks are well considered and balanced, is not a good way to live life. The purpose of wealth (my opinion) is to enhance enjoyment / happiness. If the path to get there is miserable, it is pretty irrational |

|

|

|

|

|

22 March 2024, 11:28 PM

|

#47 | |||

|

2025 Pledge Member

Join Date: Nov 2012

Real Name: Steven

Location: Glocal

Posts: 21,637

|

Quote:

Since the Fed is still targeting 2% annual currency devaluation (a.k.a. "inflation"), which is a staggering ~25% currency devaluation every 10 years.... Time itself will sort this all out, eventually. Quote:

Quote:

During the 2007/08 banking / financial scam, Evelyn de Rothschild said during a CNBC interview that for safety you hold on to gold bars. It is interesting to know that Central Banks are still purchasing gold bars too

__________________

__________________ Love timepieces and want to become a Watchmaker? Rolex has a sensational school. www.RolexWatchmakingTrainingCenter.com/ Sent from my Etch A Sketch using String Theory. |

|||

|

|

|

|

22 March 2024, 11:31 PM

|

#48 | |

|

"TRF" Member

Join Date: Jun 2023

Location: USA

Posts: 1,690

|

Quote:

I think the typical home size has increased by much more than 50% since the 80s. Home ownership over that period is virtually unchanged. Luxury vehicle market share (based on brands/types) has increased dramatically as well. I think Mercedes and BMW share today is a multiple of what it was 30-40 years ago. Nevermind other consumption items. Maybe people can just consume a bit less and enjoy things a bit more? Housing today IS expensive in many parts of the world - not unique to the US and in fact much worse in most developed countries. But comparing apples to apples for home size, I think wed find a different answer overall. Of course if youre talking Newport Beach or something, there are pockets that are outliers but as a whole I am not sure the data supports the idea people are financially worse off. Perhaps psychologically / other aspects? Maybe |

|

|

|

|

|

22 March 2024, 11:35 PM

|

#49 | |

|

"TRF" Member

Join Date: Feb 2017

Location: USA

Posts: 4,416

|

Quote:

|

|

|

|

|

|

22 March 2024, 11:46 PM

|

#50 | |

|

2025 Pledge Member

Join Date: Nov 2012

Real Name: Steven

Location: Glocal

Posts: 21,637

|

Quote:

With a probable War Economy coming, what would you suggest?

__________________

__________________ Love timepieces and want to become a Watchmaker? Rolex has a sensational school. www.RolexWatchmakingTrainingCenter.com/ Sent from my Etch A Sketch using String Theory. |

|

|

|

|

|

22 March 2024, 11:48 PM

|

#51 | |

|

"TRF" Member

Join Date: Feb 2017

Location: USA

Posts: 4,416

|

Quote:

|

|

|

|

|

|

22 March 2024, 11:48 PM

|

#52 | |

|

"TRF" Member

Join Date: Dec 2006

Real Name: D'OH!

Location: Kentucky

Watch: Rolex-1 Tudor-3

Posts: 36,310

|

Quote:

dP

__________________

TRF Member# 1668 Bass Player in TRF "AFTER DARK" Bar & NightClub Band  Commander-in-Chief of The Nylon Nation  The Crown & Shield Club Honorary Member of P-Club |

|

|

|

|

|

23 March 2024, 12:09 AM

|

#53 | |

|

"TRF" Member

Join Date: Dec 2021

Location: Asia

Posts: 887

|

Quote:

A lot of the people I still keep in touch with in the US have good careers (ie. doctors lawyers tech etc.) and they all say there is no way their kids can afford to buy a house unless they help them out with the down payment. That is maybe even more true here in Singapore where people starting out can barely even afford to rent let alone save up for a house. You either have to continue living with your parents and try to save up or hope you are lucky enough to have parents with the means to help you out. I agree about the luxury items though. I remember growing up my parents had some station wagon with wooden panels all around lol. We were never able to afford any fancy cars but life was still awesome and we were comfortable. I guess to me it just doesn't feel the same as it used to. Everyone throws around 3-5% inflation numbers but when you go out to eat or buy groceries now it's never just a 3-5% increase in prices since Covid... it's more like 30-50% or more. Maybe the internet amplified things since it made information so much more accessible and people are more likely to complain than to say how good they have it. It makes me feel really lucky and grateful for what I have today. I think if I were to start out now vs. 20 something years ago I probably wouldn't be in the same place. |

|

|

|

|

|

23 March 2024, 12:10 AM

|

#54 | |

|

2025 Pledge Member

Join Date: Nov 2012

Real Name: Steven

Location: Glocal

Posts: 21,637

|

Quote:

So.... go long Hooser / Hankook R compound tire 'futures' ;) ...and i really should bow out of this thread / threads like this. It's not you/TRF... it's me.

__________________

__________________ Love timepieces and want to become a Watchmaker? Rolex has a sensational school. www.RolexWatchmakingTrainingCenter.com/ Sent from my Etch A Sketch using String Theory. |

|

|

|

|

|

23 March 2024, 12:17 AM

|

#55 | |

|

"TRF" Member

Join Date: Jun 2016

Location: USA

Watch: All Rolex

Posts: 7,024

|

Quote:

|

|

|

|

|

|

23 March 2024, 12:24 AM

|

#56 | |

|

"TRF" Member

Join Date: Jun 2016

Location: USA

Watch: All Rolex

Posts: 7,024

|

Quote:

|

|

|

|

|

|

23 March 2024, 12:25 AM

|

#57 | ||

|

2025 Pledge Member

Join Date: Jul 2013

Real Name: Brian (TBone)

Location: canada

Watch: es make me smile

Posts: 79,357

|

Quote:

Quote:

If you believe in the capital markets, the trend is your friend, and the chart doesnt lie. Obviously there will be a correction at some point I have no doubt. Could be 10% could be 20%, I have no idea. There have been many over the years, but they appear as blips in time. The market will digest whatever the bad news is and eventually it will continue its upward trajectory. If it doesnt then we all have bigger things to worry about. There are a lot of smart people out there and some folks say they know how to outsmart the market by selling to avoid the dips and buying back in when the market is at a low. Just tune into any business news channel and listen to the talking heads they know best

|

||

|

|

|

|

23 March 2024, 01:20 AM

|

#58 | |

|

"TRF" Member

Join Date: Jun 2023

Location: USA

Posts: 1,690

|

Quote:

Expectations are not based on absolutes but instead things are relative and people re-anchor quickly and subconsciously. I grew up without cable TV. Fox viewing positions was a real thing in my house (yes, when watching Married with Children). When I started making $$ getting cable TV was a big deal. Basic cable - nothing extravagant. But it was already below the baseline for everyone I knew. My family was about 15 years behind, even in our income bracket. Fast forward a few years and I was an early adopter of streaming. Then added another service, and another. Total spend well below cable TV having multiple streaming services is now the baseline. 99% market penetration in the US. The baseline has changed you can still get local stations with a minimal one time cost (a digital antenna) with more stations and higher quality - free - vs what I had growing up. But no-one opts to. Even the bottom 5% by income This is one example but there are countless. I raised median home size because it gets obscured by the median financial data (median prices). But if someone wants to buy or build smaller, the possibility exists. Im not an optimist or pessimist. I can be cynical - but I like to ground analysis in facts, and within the context of human psychology. |

|

|

|

|

|

23 March 2024, 01:20 AM

|

#59 | ||

|

"TRF" Member

Join Date: Aug 2019

Real Name: Phillip

Location: Right here

Watch: SD43 Daytona Blusy

Posts: 2,173

|

Quote:

Quote:

|

||

|

|

|

|

23 March 2024, 04:09 AM

|

#60 | |

|

2025 Pledge Member

Join Date: Nov 2012

Real Name: Steven

Location: Glocal

Posts: 21,637

|

Quote:

PS: Almost visited Sebring to see some of the F2k guys. Lemme know via DM if/when you go there. PPS: Thx for the kind words, am bailing from the financial talk. Plus it's pretty obvious the direction and intentions. Wishing everyone the best

__________________

__________________ Love timepieces and want to become a Watchmaker? Rolex has a sensational school. www.RolexWatchmakingTrainingCenter.com/ Sent from my Etch A Sketch using String Theory. |

|

|

|

|

|

| Currently Active Users Viewing This Thread: 1 (0 members and 1 guests) | |

|

|

*Banners

Of The Month*

This space is provided to horological resources.

Linear Mode

Linear Mode